.png)

.png)

Table Of Contents

On May 22, 2025, the U.S. House of Representatives passed a legislative juggernaut, the One Big Beautiful Bill Act (OBBBA), which is already headed to the Senate for potentially additional revisions. With a razor-thin 215–214 vote margin, this sweeping bill, championed by President Donald Trump, reshapes tax laws, government spending, and economic policy.

While some are calling it a win for working-class America, real estate fund sponsors and investors need to dig deeper. Behind the headlines lies a bundle of tax tweaks and regulatory changes that could dramatically alter the real estate investment world.

Whether you’re a general partner raising capital, a limited partner seeking yield, or just someone trying to understand how D.C. decisions ripple through the property markets, this is your deep dive into what OBBBA means for real estate funds.

In this article, I’ll examine the critical provisions that will reshape investment strategies, tax optimization approaches, and capital deployment decisions across the real estate fund sector in simple terms.

The QBI Deduction Gets a Facelift: Pass-Throughs Win Big

Let's start with one of the bill's most important changes for real estate pros: the extension and expansion of the Qualified Business Income (QBI) deduction.

Understanding the Pass-Through Foundation

In the U.S., many small businesses and real estate sponsors operate as "pass-through entities" (think LLCs, S-corporations, or partnerships). Instead of the business paying taxes directly, profits "pass through" to the owners, who report that income on their personal tax returns.

This structure became the backbone of real estate investing because it avoids double taxation while maintaining operational flexibility. Most syndications and fund structures rely on this pass-through model to maximize investor returns.

Why QBI Was Created - And Why It Mattered

The QBI deduction emerged from the 2017 Tax Cuts and Jobs Act as a response to corporate tax cuts. When lawmakers slashed corporate tax rates from 35% to 21%, they needed to provide comparable relief to pass-through entities that couldn't benefit from the corporate rate reduction.

The solution was elegant: allow eligible taxpayers to deduct up to 20% of their qualified business income, reducing their effective tax rate and boosting cash flow. For real estate investors, this became a powerful tool that didn't require restructuring their existing entities.

The Catch: Restrictions That Complicated Planning

But this tax benefit brought a new level of tax planning complexity. The deduction included limits based on income thresholds, industry type, and how much a business paid in wages or owned in qualified property. Professionals in fields like law, accounting, and consulting often faced restrictions, especially if their income exceeded certain thresholds.

I've worked with fund sponsors who had to carefully structure their operations to qualify for maximum QBI benefits. The temporary nature of the deduction (set to expire at the end of 2025) created additional planning challenges and uncertainty around long-term fund strategies.

OBBBA's Game-Changing Enhancement

This is where OBBBA transforms the equation. The bill doesn't just extend the QBI deduction - it makes it permanent and increases it from 20% to 23% [Source]. This removes the uncertainty that has plagued investment planning since 2017 while providing even greater tax benefits.

For real estate fund sponsors, this permanent enhancement means they can now build long-term investment strategies around QBI optimization without worrying about expiration dates. The 3% increase may seem modest, but it compounds significantly across large fund portfolios.

Real-World Impact on Investment Decisions

I expect this change will reshape how sponsors structure their funds and market to investors.

For investors, syndications and other pass-through structures that generate QBI become substantially more appealing. This could drive increased competition for quality real estate deals as more capital flows toward tax-efficient investment structures.

Plain Talk: If you invest in a real estate partnership that makes a profit, this deduction reduces the income you pay taxes on. That means you keep more of your money, and now it's a permanent benefit you can count on.

SALT Deduction Cap Raised: Relief for High-Tax States

Next up: SALT. That's short for "State and Local Taxes," and it refers to the taxes you pay to your state or city government.

Historical SALT Deduction Framework

Historically, you could deduct these payments from your federal tax bill within your itemized deductions (think: Schedule A). This provided meaningful tax relief for investors with substantial state and local tax obligations.

2017 Tax Law Impact

Under Trump's 2017 tax law, the SALT deduction was capped at $10,000, at the same time that the competing standard deduction was raised. This dual change made the SALT deduction much less meaningful for most taxpayers, particularly those in high-tax jurisdictions.

OBBBA's SALT Cap Modification

The latest version of OBBBA changes that by raising the SALT cap to $40,000, starting in 2025. But it comes with a catch: for taxpayers earning over $500,000, the deduction gradually phases out.

The cap increases 1% each year, which means a little more breathing room for high-income earners over time.

Strategic Impact on Real Estate Investment

For real estate investors in high-tax states like New York, California, and New Jersey, or for those with significant property tax costs, this is a game-changer.

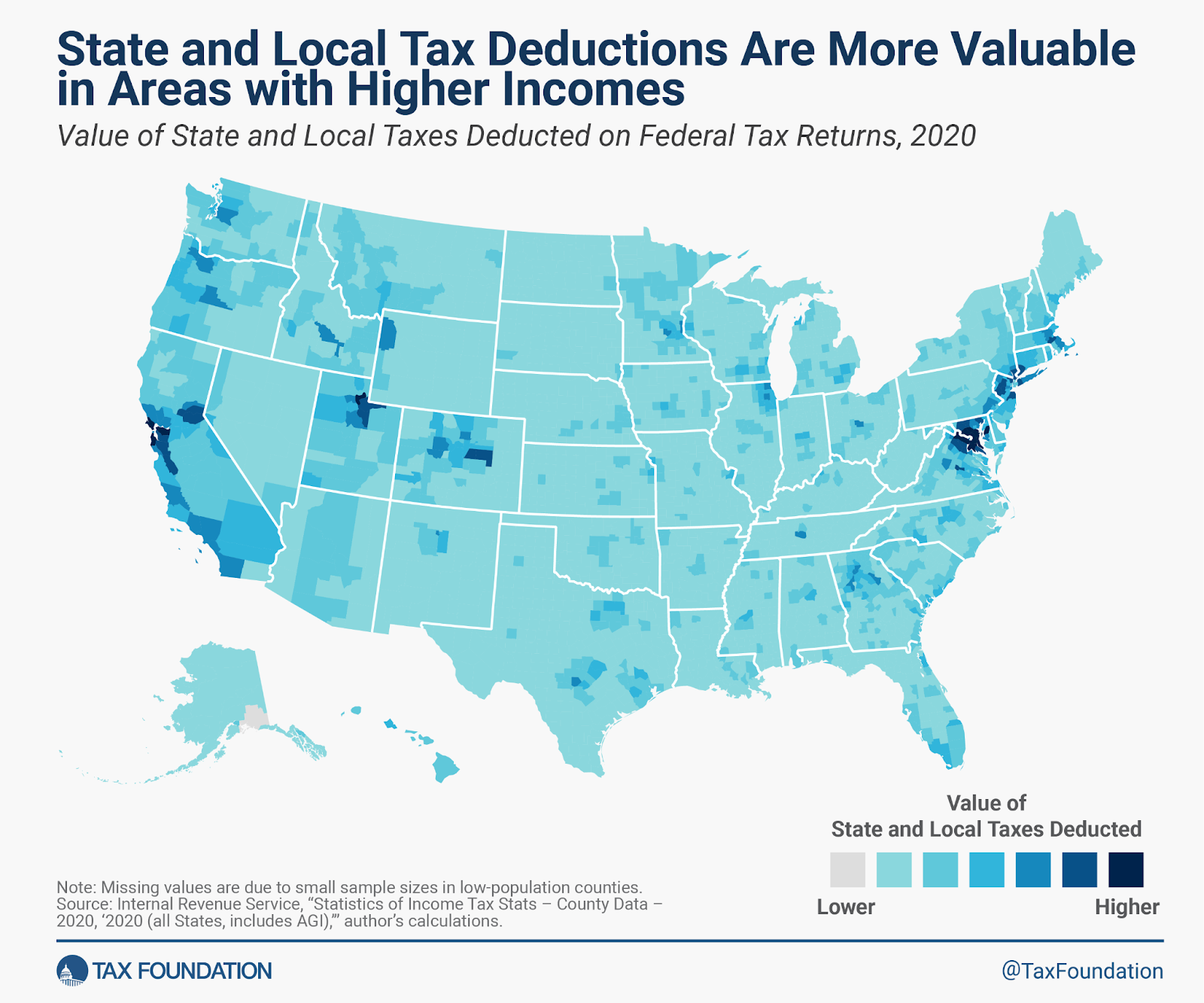

As this Tax Foundation data shows, SALT deductions were heavily concentrated in coastal markets before the 2017 cap, exactly the areas that will benefit most from OBBBA's increase to $40,000.

When you combine the increased SALT deduction with the beefed-up QBI deduction, the after-tax yield on real estate investments can achieve a solid bump. I expect this will shift investor interest back toward markets that became less attractive after the 2017 SALT cap implementation.

Plain Talk: More of your income stays in your pocket, making real estate syndications and fund investments more attractive, especially for those frustrated by high state or local taxes.

Business Interest Deduction Relief: The Hidden Win for Fund Efficiency

One of the most quietly impactful changes in OBBBA is how it reshapes the rules around business interest deductions, specifically, the Section 163(j) limitation.

The Election Dilemma That's Been Plaguing Sponsors

For the last few years, many real estate sponsors have had to make a difficult trade off - elect out of the cap to fully deduct interest, but live with the downside: longer ADS depreciation schedules and losing out on bonus depreciation for certain property types. That election didn't kill bonus depreciation entirely, but it narrowed its reach significantly.

OBBBA's EBITDA-Based Solution

Now, with OBBBA reverting to an EBITDA-based cap through 2029, the pressure to make that election eases substantially. Most funds will be able to deduct more interest without giving up the depreciation benefits that make our models work.

Real-World Implementation Benefits

What does that mean in practice? Smoother 1065s. No more toggling between cost segregation and ADS schedules. More bonus depreciation stays on the table, and more interest expense stays deductible. LPs see stronger paper losses on their K-1s, and sponsors can get back to structuring deals around what works, not what avoids a tax limitation.

This isn't just a cleanup of the rules, it's a real opportunity to enhance fund efficiency without sacrificing flexibility. OBBBA doesn't eliminate complexity, but for once, it's cutting us some slack instead of tightening the screws.

Plain Talk: Your fund's tax filings get simpler, your interest deductions get bigger, and you don't have to sacrifice depreciation benefits to make it work. It's a rare win-win in the tax code.

Clean Energy Tax Credits Slashed: ESG Strategies Hit a Wall

Here's where the train gets a bit wobbly, especially for those invested in green real estate projects.

The Credits That Made Green Building Profitable

The OBBBA significantly cuts back on clean energy tax credits, like the Investment Tax Credit (ITC) and Production Tax Credit (PTC). These were key tools for real estate developers building energy-efficient projects like solar panels, green HVAC systems, LEED-certified buildings, and more.

Take the ITC, for example. Until recently, it offered a 30% tax credit on qualifying energy systems like solar or geothermal [Source]. That meant if you spent $1 million on rooftop solar, you got $300,000 back as a credit. The PTC, meanwhile, gave a per-kilowatt-hour benefit for renewable electricity generation over a decade, which added up fast on larger projects.

Together, these programs made green building financially feasible, even profitable.

OBBBA's Aggressive Timeline Crunch

Fast forward to now, OBBBA slashes those benefits with a much earlier expiration date. Most of these credits are now set to disappear by 2029, three years sooner than originally planned. Even more urgent: only projects that break ground within 60 days of the bill becoming law can still qualify.

And let's be honest, that's almost impossible. Getting permits, locking in financing, ordering equipment, and lining up your contractors? That takes months, not weeks. For developers with green ambitions, this abrupt deadline is a logistical nightmare.

The Real Numbers Behind the Impact

Let's look at the numbers now. Say you're building a 100-unit apartment complex and budgeting a million dollars for solar. Pre-OBBBA, you'd shave off $300,000 with the ITC. Now? That money's gone. You're eating the full cost unless you can find some local incentive to fill the gap.

That might be doable in places like California or New York, but good luck if you're in Texas or Arizona, where state-level support is limited or nonexistent.

ESG Fund Strategy Disruption

It doesn't stop there. Think about ESG-branded funds; those that promise investors environmental impact along with returns. If you were planning to certify a $100 million office project to LEED Gold, you might be looking at an extra $2–5 million in costs for energy-efficient design and construction.

That's a tough pill to swallow without federal tax breaks to soften the blow. Now, fund managers have to go back to their LPs and say, "We're still green, but the numbers are tighter." Some investors will understand. Others won't.

The Strategic Pivot Requirement

This shift doesn't just affect budgeting. It changes the whole narrative around sustainable real estate. ESG used to be a smart way to differentiate your fund and attract capital. Now, without federal backing, it's riskier.

You either find new ways to make the numbers work, or you pivot quickly. Some sponsors may downplay their green ambitions. Others will double down and get creative, leveraging local programs, utility incentives, or even tenant demand for environmentally friendly spaces.

I see this as a real inflection point. It forces sponsors and investors to take a hard look at how they define "sustainability" in the absence of federal support. It raises the bar for project feasibility and increases the pressure to deliver returns in a tighter, less subsidized environment.

The Two-Fold Challenge

The proposed bill, therefore, creates a two-fold issue:

- Higher upfront costs for sustainable construction

- A time crunch to get green projects started before the window closes

If your business model relies on generous clean energy credits, it's time to adapt or risk being left behind.

Impact: ESG-focused investors and developers may have to pivot quickly, either shelving green plans or relying on state-level incentives, which aren't always as generous.

Plain Talk: If your fund pitches a sustainable strategy, be ready to show investors how you'll adapt. And don't bank on federal credits to pencil out your project anymore.

Tax Breaks for Tips and Overtime: Construction Gets a Boost

The bill introduces another tax incentive, this time aimed at the workforce. OBBBA proposes exempting tips and overtime pay from federal income taxes.

That might sound like a small worker-friendly perk, but it has broader implications. For real estate developers and value-add operators juggling delayed construction timelines and labor shortages, this provision could help speed things up.

Construction Worker Incentive Structure

If construction workers can decrease their federal taxes on working overtime, they're more likely to put in extra hours. That can lead to faster turnarounds, earlier lease-ups, and better overall IRRs (Internal Rate of Return) for project sponsors.

Implementation Uncertainties

There is a caveat: the rules around this exemption are still being debated, and predicting how workers will respond is tricky. But if implemented, it could help ease project timelines, especially in markets with labor bottlenecks.

I see this as particularly beneficial for projects operating under tight delivery schedules in competitive labor markets.

Plain Talk: Faster builds equal faster cash flows. A big win if you're on the clock for a value-add or ground-up deal.

Bonus Depreciation Restoration: Capital-Intensive Project Optimization

One of the most under-the-radar, but potentially game-changing provisions of OBBBA is the return of 100% bonus depreciation.

Bonus Depreciation Mechanism and Application

For those unfamiliar, bonus depreciation allows you to immediately write off the full cost of qualifying assets in the year they are placed in service, rather than depreciating them over time. This is a huge deal in real estate, where upfront costs for improvements, fixtures, and equipment can be significant.

OBBBA's 100% Bonus Depreciation Restoration

Before OBBBA, bonus depreciation was set to phase down to 40% in 2025, continuing to decline in the years ahead. This created planning uncertainty and reduced immediate tax benefits for capital-intensive real estate projects.

The bill restores full 100% bonus depreciation for property acquired after January 19, 2025, and placed in service before January 1, 2030. That gives sponsors a five-year runway to make major capital improvements and reap immediate tax savings.

Key Implementation Parameters:

- Acquisition threshold date: January 19, 2025

- Service placement deadline: January 1, 2030

- Depreciation percentage: 100% immediate write-off

- Strategic planning window: Five-year optimization period

Case Study: Value-Add Renovation Tax Impact

Say you're planning a value-add renovation on a 200-unit apartment complex and you spend $2 million on upgrades that qualify for bonus depreciation. Under the old rules, you might have only deducted $800,000 in the first year.

With OBBBA's reinstated 100% bonus depreciation, you can deduct a large portion of the $2 million in year one under a cost segregation study. That can mean tens, or even hundreds of thousands of dollars in tax savings, depending on your structure.

Strategic Implementation Through Cost Segregation

The key to maximizing these benefits lies in proper cost segregation implementation. I've detailed the complete strategy and implementation timeline in my comprehensive guide: Why Real Estate Funds Should Act Fast on Cost Segregation in 2025.

For funds, this translates into higher first-year returns, more distributable cash flow, and greater appeal to tax-conscious investors. It also gives sponsors a tool to shield gains from sales or refinancing, making timing and exit strategy even more critical.

Plain Talk: This is a powerful planning opportunity for fund managers, and one that shouldn't be overlooked. If you've been holding off on improvements or acquisitions because of tax concerns, the door just opened wide.

Strategic OBBBA Implementation: Getting Professional Help

The complexity of OBBBA's tax changes means you'll need specialized expertise to capture the full benefits. Enhanced QBI deductions, restored bonus depreciation, and modified SALT caps create real opportunities, but only when implemented correctly.

At SponsorCloud, my team and I have worked with over 1,000 fund managers representing $10B+ in investor capital to maximize their after-tax returns through strategic tax planning. Our integrated approach often increases the after-tax IRR by up to 2.5% for clients who implement these strategies properly.

Based on what I'm seeing with OBBBA's changes, here's what fund managers need to focus on immediately:

- Fund Structure Review: Evaluate your current setup for maximum QBI benefits under the new rules.

- Green Project Assessment: Figure out which sustainable projects still make sense without federal credits.

- Marketing Updates: Highlight your tax efficiency advantages to attract savvy investors.

- Timing Strategy: Accelerate acquisitions to capture bonus depreciation within the five-year window.

We've helped clients navigate similar legislative changes before, and the results speak for themselves:

- $10M EUM Fund: Resolved IRS audit complications, implemented multi-state tax strategies, restored investor confidence.

- $40M EUM Fund: Reduced penalties by 84% through integrated amnesty programs and proactive compliance frameworks.

- $150M EUM Fund: Delivered $1M+ annual tax savings through comprehensive optimization protocols; enhanced investor satisfaction metrics.

How We Help: Our team of CPAs and tax strategists works directly with fund managers to turn OBBBA's benefits into real investor returns. We handle the technical complexity so you can focus on finding deals and managing relationships.

If you're serious about maximizing OBBBA's opportunities, professional guidance isn't optional, it's essential.

Schedule a Consultation to see how we can help you implement OBBBA strategies tailored to your fund.

Final Thoughts

The "One Big Beautiful Bill Act" is more than just a political talking point. It signals a new era of tax policy that could tilt the playing field for real estate fund sponsors and investors alike.

On the plus side, we get a stronger QBI deduction, more generous SALT caps, and potential labor tailwinds. On the flip side, the dismantling of clean energy credits means higher costs for sustainable projects and less federal support for ESG-driven strategies.

And if you're an investor? Look for managers who understand the nuances of this bill and can help you maximize after-tax returns in this new landscape.

%201%20(1).svg)