.png)

.png)

Table Of Contents

The foundation of every successful fund rests on a critical decision that many managers overlook: selecting the right legal structure. This decision affects everything from tax treatment and investor relations to administrative costs and growth potential.

In our recent webinar with LegalScale, we explored the nuances of LP, LLC, and Series Fund structures. As someone who works with fund managers daily on tax and administrative considerations, I wanted to share these insights to help you make informed decisions for your next fund.

Why Structure Matters Beyond Legal Documentation

When discussing fund structures, we often focus solely on legal documentation. However, structure selection impacts far more than paperwork. Your choice will determine:

- Which investors you can attract

- Your tax obligations and those of your investors

- Administrative costs and complexities

- Your ability to scale efficiently

The right structure creates a solid foundation for growth, while the wrong one introduces friction that can hinder performance and increase expenses.

As Neil O'Donnell from LegalScale pointed out during our webinar:

"The type of funds and the type of fund structure that we choose can impact the investors that we can solicit, the perspective liability for those investors and the investment manager. It can impact tax treatment, especially for foreign tax and for tax-exempt investors. And it can impact governance."

LP, LLC, or Series Fund: Understanding Your Options

Let's examine each structure and its tax and administrative implications:

Limited Partnership (LP): The Industry Standard

The LP structure remains the gold standard for institutional investors, particularly for private equity, venture capital, and hedge funds. Its familiarity brings comfort to sophisticated investors who expect this traditional framework.

From a tax perspective, LPs offer pass-through taxation, meaning there's no entity-level tax. Instead, profits and losses flow directly to partners who report them on their individual returns. This structure appeals to tax-exempt and institutional investors who value transparency.

However, the LP structure does have administrative considerations:

- General Partners (GPs) have fiduciary duties and personal liability

- Requires more formal setup, including creating a GP LLC

- Limited Partners must remain passive to maintain their limited liability

- Often requires separate entities for asset holdings

Limited Liability Company (LLC): The Flexible Alternative

LLCs provide more flexibility than the traditional LP structure. All members enjoy limited liability protection, and management structures can be tailored to your specific needs.

From a tax perspective, LLCs offer remarkable versatility:

- Default partnership taxation (pass-through)

- Option to elect S-Corporation taxation (potential self-employment tax benefits)

- Option to elect C-Corporation taxation (for specific situations)

This flexibility makes LLCs popular for smaller funds or closely held structures where investors might want more input through side letters or operating agreements.

Series LLC/Fund: The Efficiency Solution

Series funds represent a newer option for managers looking to launch multiple strategies or accounts under one umbrella. A master LLC entity houses multiple series, each with separate assets and liabilities.

The administrative benefits can be substantial:

- One master legal filing with simpler documentation for each series

- Reduced formation costs and ongoing legal expenses

- Ability to launch new strategies quickly

However, from a tax perspective, series funds create unique complexities:

- May be treated as a single entity for federal tax purposes

- Often treated differently at state levels

- Can create state-specific tax risks

- May require separate bank accounts for each series

These structural basics form the foundation, but practical implementation involves additional considerations. Neil O'Donnell explores these nuances in the following segment, including Delaware statutory trusts and specific liability protections for each structure type:

Administrative Considerations for Each Structure

Here are the administrative requirements that you should factor into your decision:

Formation Complexity

Formation complexity varies by structure:

- LPs require more formal documentation. (LPA, GP formation)

- LLCs are typically simpler to form, but require careful drafting of operating agreements.

- Series LLCs have moderate formation complexity with the master entity, but simplified documentation for each series.

Ongoing Administration

Each structure creates different administrative burdens:

- LPs have standardized reporting, but require maintaining GP/LP separation.

- LLCs offer flexibility but may require more customized governance.

- Series LLCs simplify documentation but add complexity for maintaining separate series records.

Investor Familiarity

Investor comfort with different structures varies significantly:

- LPs are highly familiar to institutional investors.

- LLCs are moderately familiar, especially to smaller investors.

- Series LLCs have lower familiarity and may require additional investor education.

Jurisdictional Considerations

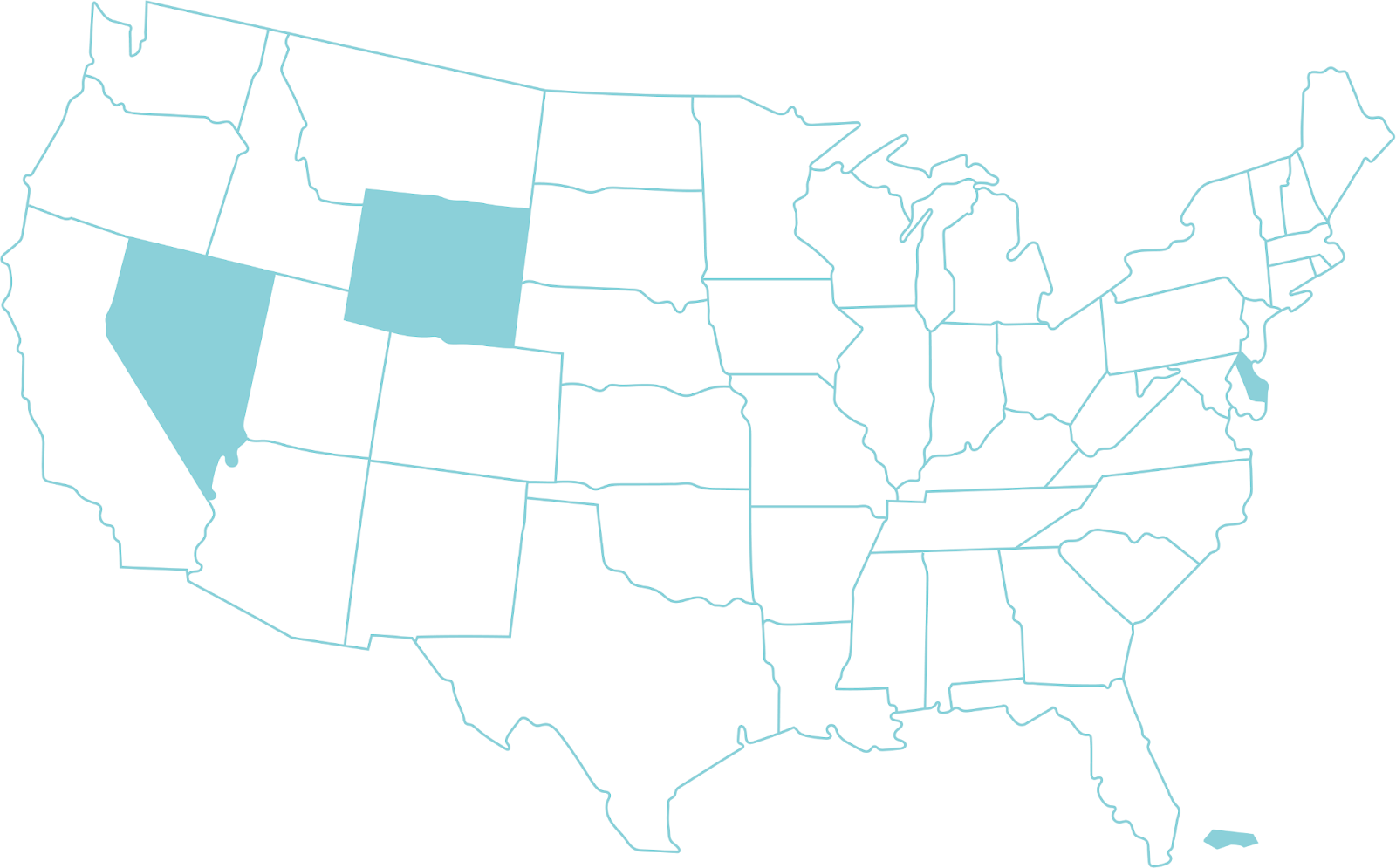

Where you form your entity matters as much as which type you choose. Popular jurisdictions include:

Delaware: The Standard for Institutional Funds

Delaware remains the preferred jurisdiction for institutional-quality funds because it offers:

- Well-established case law.

- Business-friendly environment.

- Sophistication in handling complex fund structures.

- Special advantages for real estate (Delaware Statutory Trusts)

Neil specifically highlighted Delaware's advantages for real estate:

"Delaware tends to be a place where commercial real estate rules and managers have special rights, and we can create a Delaware Statutory Trust, and those DSTs can have special corporate protections applied to them. So Delaware, especially for commercial real estate reasons, is a preferred jurisdiction."

Wyoming and Nevada: Alternative Domestic Options

Wyoming and Nevada provide alternatives with specific benefits:

- Wyoming offers lower costs and faster processing.

- Nevada provides strong asset protection and anonymity.

- Both have charging order protections for members.

Cayman Islands: International Standard

For international investors, Cayman Islands entities remain standard because they:

- Provide tax neutrality.

- Have a strong banking infrastructure.

- Maintain strong tax treaties.

- Are familiar to international investors.

Tax Implications That Drive Structure Decisions

Tax considerations stand among the most important factors when selecting a fund structure. Let's look at the implications for each:

Pass-Through Taxation Benefits

Both LPs and LLCs (by default) operate as pass-through entities. This means:

- No entity-level taxation

- Profits and losses flow directly to investors

- Each investor receives a Schedule K-1

- Tax attributes maintain their character (capital gains, ordinary income, etc.)

For most domestic fund situations, pass-through taxation offers advantages by avoiding double taxation and allowing tax attributes to flow to investors.

Entity-Level Taxation Considerations

When an LLC elects to be taxed as a C-Corporation, it creates entity-level taxation. While this typically results in double taxation (corporate and shareholder level), there are specific situations where it makes sense:

- When creating blocker entities for international investors

- For tax-exempt investors concerned about Unrelated Business Taxable Income (UBTI)

- When planning exit strategies that benefit from corporate structures

International Investor Structures

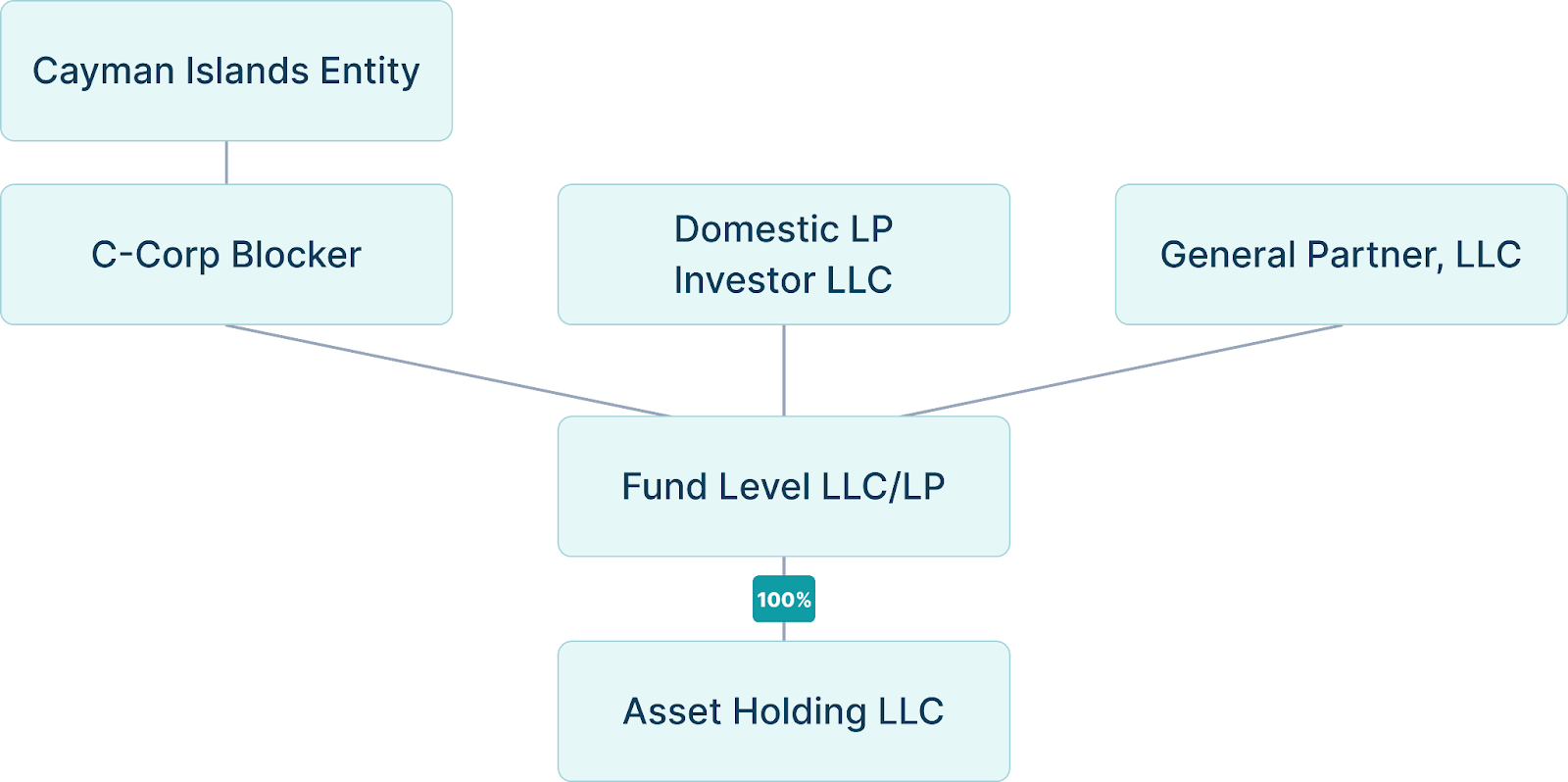

For funds targeting international investors, structure selection becomes particularly important. The standard approach involves creating:

- A C-Corporation blocker entity

- Potentially a Cayman Islands entity for additional tax benefits

This structure provides significant advantages:

- Lower withholding tax rates for foreign investors

- Reduced reporting requirements

- Protection from FIRPTA for real estate investments

- Tax treaty benefits

Tax implications extend beyond these fundamental considerations. The following webinar segment covers additional optimization strategies, including S-Corp elections within LLCs and navigating SEC compliance requirements for different structures:

Common Fund Structures in Practice

Theory is helpful, but seeing structures in action provides a better understanding. Let's examine some common structures we implement for clients:

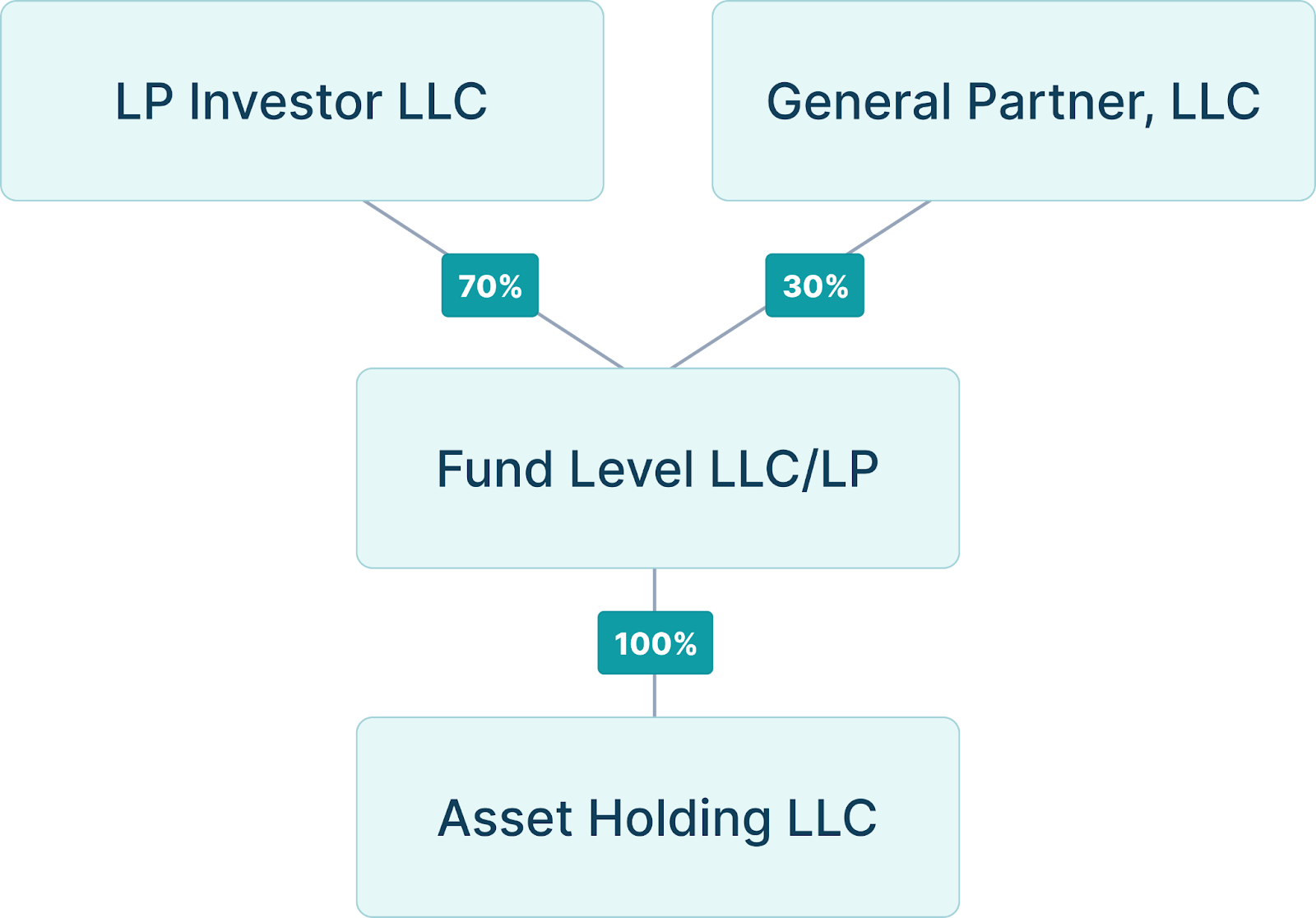

Domestic Fund Structure

For most domestic funds, we typically see the following structure:

- Asset holding LLC(s) at the bottom (usually single-member LLCs)

- Fund level LLC or LP in the middle

- LP investor LLC and GP investor LLC at the top

This separation serves several purposes:

- Isolates liability between assets and the fund

- Creates clean governance lines

- Allows for appropriate profit/loss sharing (typically 70/30 in favor of LPs)

- Simplifies administration for multiple assets

Global Fund Structure with International Investors

When including international investors, the structure typically expands to include:

This structure effectively shields foreign investors from direct U.S. tax liability while maintaining operational efficiency.

While these diagrams illustrate the conceptual framework, the practical implementation involves specific documentation flows and entity relationships. I walked through detailed examples in this segment, showing how common structure choices impact daily operations:

Special-Purpose Structures for Specific Situations

Beyond standard structures, specialized arrangements serve specific investment strategies. Here are two examples we frequently implement:

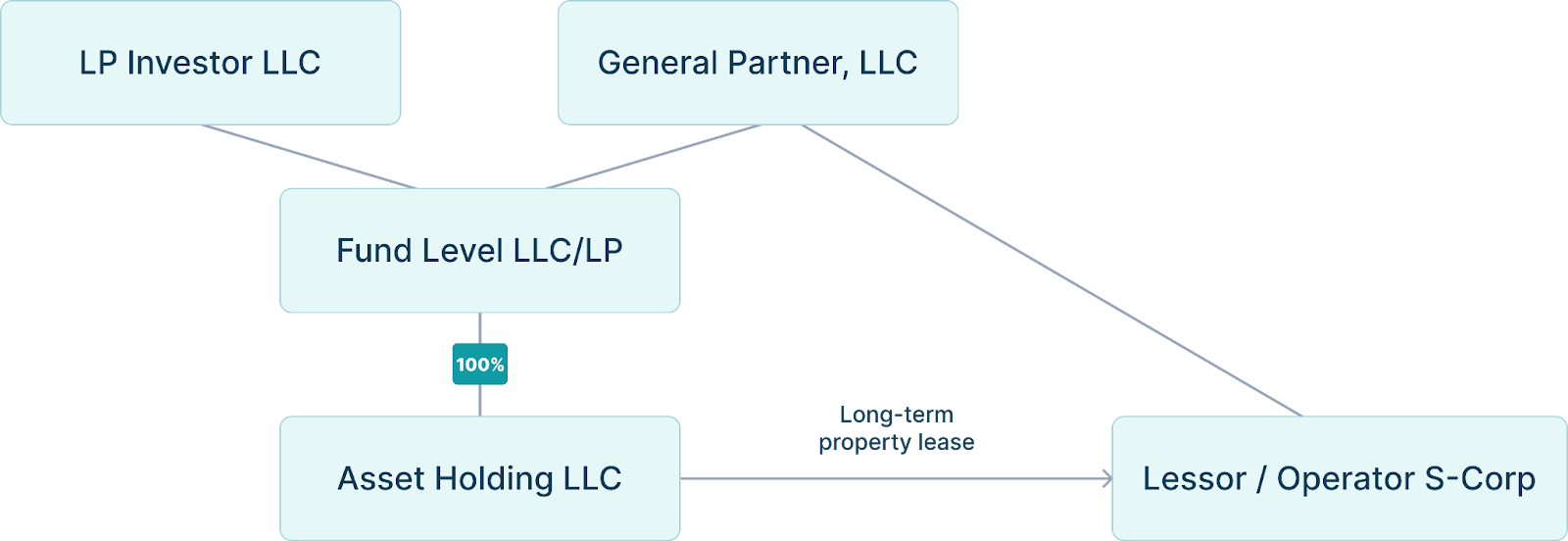

Short-Term Rental Structure

Short-term rentals (STRs) present unique tax challenges because they don't follow standard real estate tax rules. The typical structure includes:

The S-Corporation maintains the short-term rental contracts and makes a long-term lease from the fund-level LLC. This separation preserves real estate tax benefits for investors while isolating the active business aspects.

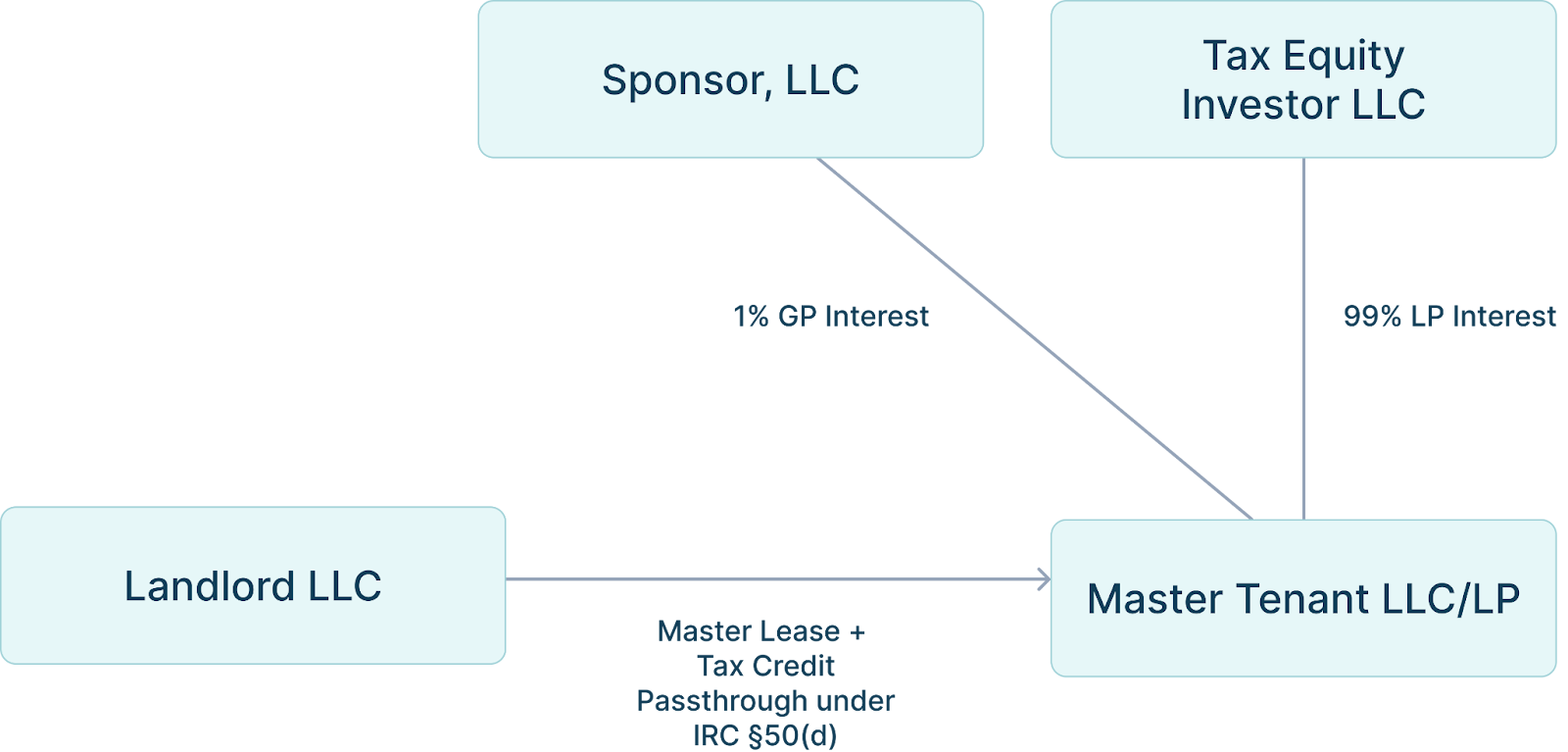

Tax Credit Investment Structures

For tax credit investments (historic, low-income housing, etc.), we create more complex structures:

This structure allows tax credits to flow to the tax equity investor while maintaining property ownership and management control.

To understand the additional considerations for STR and Tax Credit structures, including specific documentation requirements and compliance nuances, watch the segment below:

Making the Right Decision for Your Fund

After reviewing all these considerations, how do you choose? I recommend following these steps:

- Start with your investor base: Who are you targeting, and what structures do they expect or prefer?

- Consider your investment strategy: Different assets and holding periods may benefit from different structures.

- Evaluate tax implications: How will your structure affect both your fund's tax position and your investors'?

- Assess administrative capabilities: Do you have the resources to manage the reporting and compliance requirements?

- Plan for growth: Will your chosen structure support your long-term vision?

Neil emphasized this holistic approach:

"We never want the legal tail to wag the business dog. The realities of the investments, the realities of soliciting investors should drive in every instance."

Final Thoughts

There's no one-size-fits-all approach to fund structuring. The right choice aligns with your specific investor base, strategy, and administrative capabilities.

LPs remain the industry standard for good reason, particularly for larger funds targeting institutional investors. LLCs offer flexibility that works well for smaller or more closely held structures. Series funds provide efficiency for platform approaches launching multiple strategies.

To quote Neil's concluding advice:

"We want to make sure that we align with the investor base, with their expectations. Furthermore, we want to be guided by your strategy. Limited partnerships are the most standard structure, typically typifying the biggest investments, and series funds can be helpful for platform businesses that are doing one or two acquisitions at a time."

The most important advice I can offer is to consult with experienced advisors early in your planning process. Structure changes become increasingly difficult and expensive once a fund is operational.

By focusing on these considerations upfront, you'll create a foundation that supports growth rather than constraining it. Your structure should serve your strategy, not the other way around.

This article is based on insights from our recent webinar, "Choosing the Right Structure: LP vs. LLC vs. Series Fund," co-hosted with LegalScale.

We would like to thank Neil O'Donnell, Managing Partner at LegalScale, for his valuable contributions and legal expertise. Neil specializes in private equity transactions and fund formation, representing investors and emerging-growth companies with early-stage financings. His practical approach to fund structuring complements our operational focus at SponsorCloud.

LegalScale and SponsorCloud have partnered to provide fund managers with comprehensive solutions that address both the legal and operational aspects of fund management. This collaboration ensures that our clients receive expert guidance from formation through ongoing administration.

To learn more, book a consultation with us.

%201%20(1).svg)